Original article ISPreview UK:Read More

A new high-level report from Assembly Research will be published today, which examines the challenging future of the UK’s full fibre broadband market for alternative networks (altnets) and highlights the potentially positive impacts of nexfibre’s recent £2bn move to acquire rival operator Netomnia (here).

Regular readers will already be aware that altnets have faced plenty of challenges over the past few years, fuelled by strong competition (i.e. pressures from overbuilds and limited take-up), rising build costs and high interest rates. The situation has caused most altnets to make redundancies and scale-back or even stop their roll-outs of gigabit-capable broadband infrastructure in order to focus on commercialisation.

On the flip side, altnets have invested billions of pounds to help expand competitive full fibre infrastructure, which has played a not insignificant role in pushing the established players (Openreach and Virgin Media) to up their game and increase their own efforts. At the same time consumers are benefitting from the extra choices, faster speeds and lower pricing that all these services bring.

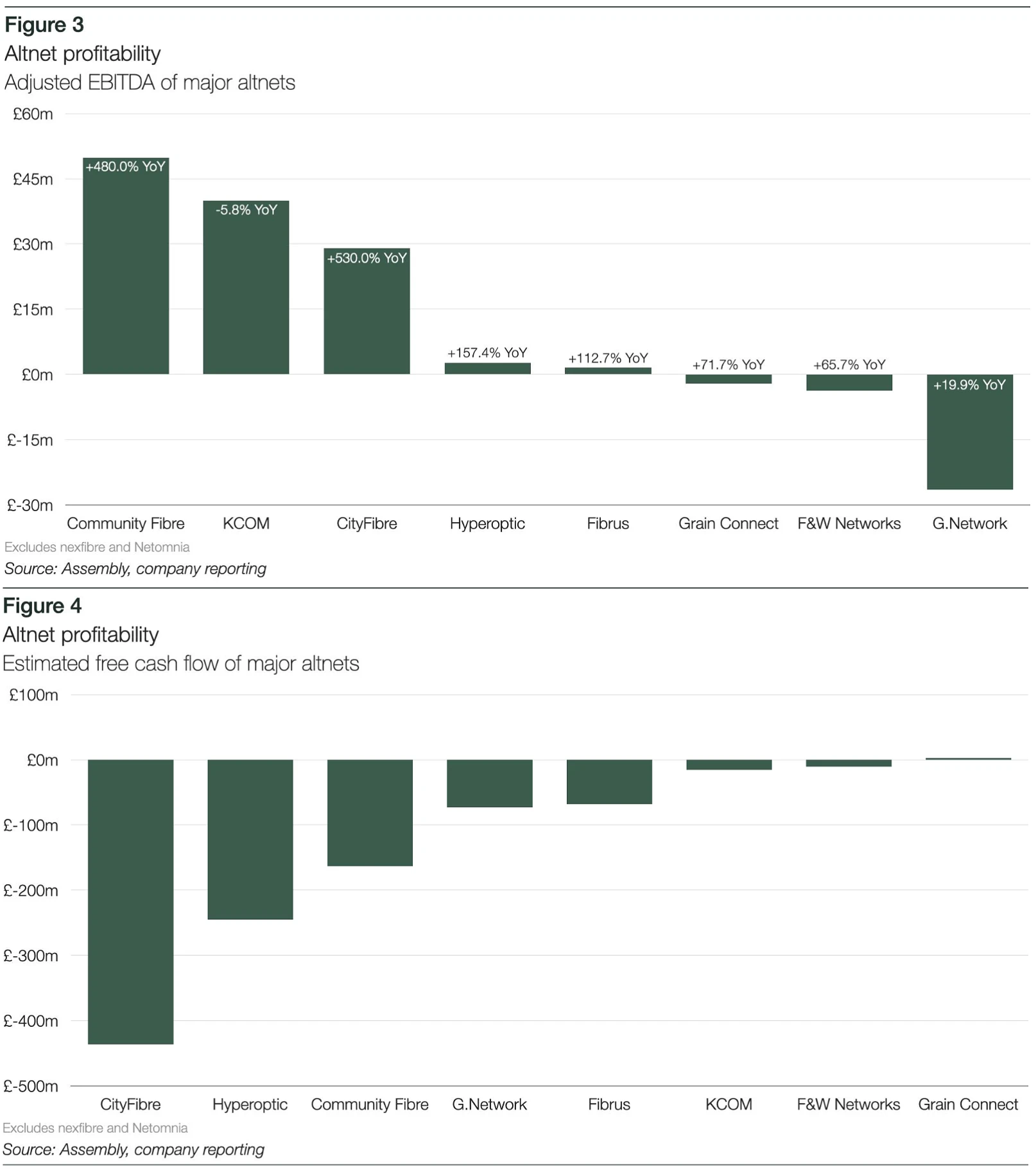

Nevertheless, the altnet market’s lack of widespread profitability has become a frequent talking point, although the report does highlight how some operators have begun to make positive progress after prioritising take-up. For example, it notes that Fibrus has achieved a take-up rate of 28% over its network (currently 30%+), CommunityFibre grew its customer base by 26% in 2025 to 429,000 (take-up rate of just under 32%), and CityFibre has reported that it had “exceeded 20% penetration across its consumer footprint and is on track to exceed 30% by the end of 2026”.

Despite these positives, the report notes that some of these larger altnets, particularly CityFibre, still have significant debt burdens hanging over them – with CityFibre’s total reported current and non-current liabilities amounting to £5.1bn. Recent financial reporting shows that some of the most significant increases in earnings before interest, taxes, depreciation and amortisation (EBITDA) have also stemmed from those larger altnets. “While five of the eight largest altnets have reported positive EBITDA figures, two of them (Hyperoptic, Fibrus) have done so narrowly,” said the report.

The study’s definition of the “largest altnets” above is, at this point, open to some debate. The above charts include the likes of Grain Connect, G.Network and F&W Networks, while at the same time leaving out Trooli, Gigaclear and FullFibre Limited (post Zzoomm merger), among others – the latter three have larger FTTP networks (we’ve been told this was due to a lack of key financial data at the time). In any case, Assembly’s report goes on to make five key points about today’s market.

Assembly’s Key Messages

1. Supportive government policy and enabling Ofcom regulation propelled the UK’s rollout of fi bre, seeing coverage increase from 17% to 78% over the last five years. Despite the contribution of altnets to this success story, build-out across the country has been more disparate than expected, with some smaller operators unlikely to survive on a standalone basis.

2. While some altnets have recorded strong revenue growth, EBITDA remains negative for three of the eight largest, with a further two only marginally profi table on this basis. Cash flow is negative for all but one altnets. Amid increasing concerns about the sustainability of many of their peers, collapse of the market could have significant implications for consumers, network competition and public funding.

3. The current fragmented nature of the market limits investment, causes unnecessary overbuild and exacerbates the issue of encouraging take-up. While nexfibre and CityFibre are the largest players behind Openreach, neither currently – nor are likely to on their own – match the incumbent’s operation. Scaled challengers are required for the long-term competitiveness of the wholesale fibre market, as well as for Openreach’s route to deregulation.

4. Consolidation is the obvious next chapter in the UK’s fibre story, initiating the transition to a more sustainable market with fewer but ultimately more financially stable operators. Ofcom and the CMA are well-placed to enable an orderly combination of assets that promotes competition and protects consumers, while driving investment and economic growth.

5. nexfibre/Netomnia reflects the type of deal needed to help establish effective and sustainable competition to Openreach for the long-term. However, a prolonged Phase 2 merger review process could have a chilling effect on investment and discourage other operators from taking the steps towards the consolidation and meaningful scale that the industry now needs.

The report then spends a few of its pages attempting to warn the Competition and Markets Authority (CMA) against proceeding to a deeper Phase 2 review of nexfibre’s deal with Netomnia, which could delay the agreement and may even require concessions (blocking the deal outright seems less likely, but not impossible). The CMA have yet to make a decision about whether to proceed with a limited Phase 1 review, let alone a Phase 2, but P1 is expected as par for the course for this sort of deal.

Assembly Research Report Extract

“Such a delay risks limiting or slowing investment into the UK’s fibre market, including the forecasted investment in domestic fibre networks that the nexfibre/Netomnia acquisition and further transactions would trigger. It could create regulatory uncertainty for the backers of other altnets, potentially discouraging them from providing new funding to fuel additional investment until the eventual outcome of the investigation is made known, with knock-on effects for GDP growth.

A lengthy Phase 2 could also risk hampering further consolidation, particularly for merging parties where the target’s revenue would be sufficient to trigger a formal CMA review, leaving ongoing scale and profitability challenges unaddressed.

Taken together, the potential chilling effect on investment and consolidation could hold up the development of sustainable infrastructure-based competition to Openreach, whether that be from a combined nexfibre/Netomnia or from another scaled altnet. This would constrain the market in its current state, limiting the flow of benefits to end users.”

Naturally, that is one viewpoint, but it’s not the only one. A recent study from Point Topic highlighted that there might also be some negatives from the deal, such as from reduced infrastructure-level competition and less aggressive consumer pricing over time in overlapping network areas (here). Lest we forget that nexfibre is not widely viewed as being a truly independent altnet, since it shares key parentage with VMO2.

The CEO of CityFibre, Simon Holden, which itself had tried to acquire Netomnia (vested interest), similarly said: “There’s an 80 percent overlap between these two players and, if the deal goes ahead, it would significantly reduce competition and the choice available to consumers, as well as force hundreds of thousands of Netomnia customers back to VMO2 … this deal risks re-establishing an ineffective duopoly of BT and VMO2 and undermining the significant progress the UK has made.”

Naturally, a market with several scale challengers to Openreach would be more ideal than a return to the duopoly of old (even if the VMO2/nexfibre side may yet deliver more open wholesale access than before), although it remains to be seen whether there’s enough consolidation flexibility left – among the remaining altnet players – to produce some truly effective competition at scale across the UK.

Big deals require big funding and, so far, nexfibre’s parents have shown they’re willing to dig deep to secure a strategic advantage. But nobody has an infinite pot of money to play with, not even nexfibre’s parents, and other altnets expecting to get a similar deal to Netomnia’s – either via VMO2/nexfibre, CityFibre or others – may be in danger of stepping into the territory of wishful thinking, when more realism is required.