Original article ISPreview UK:Read More

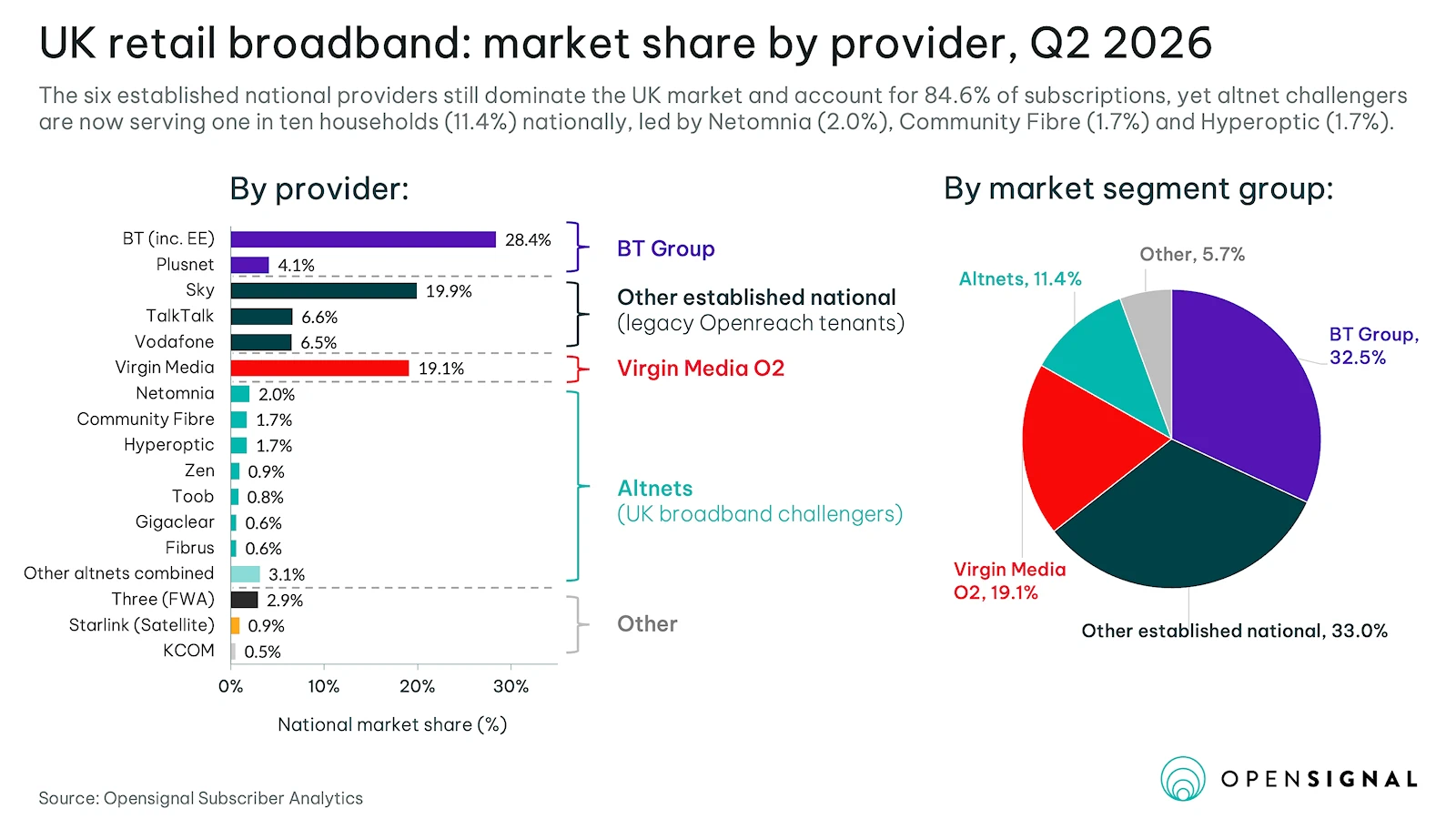

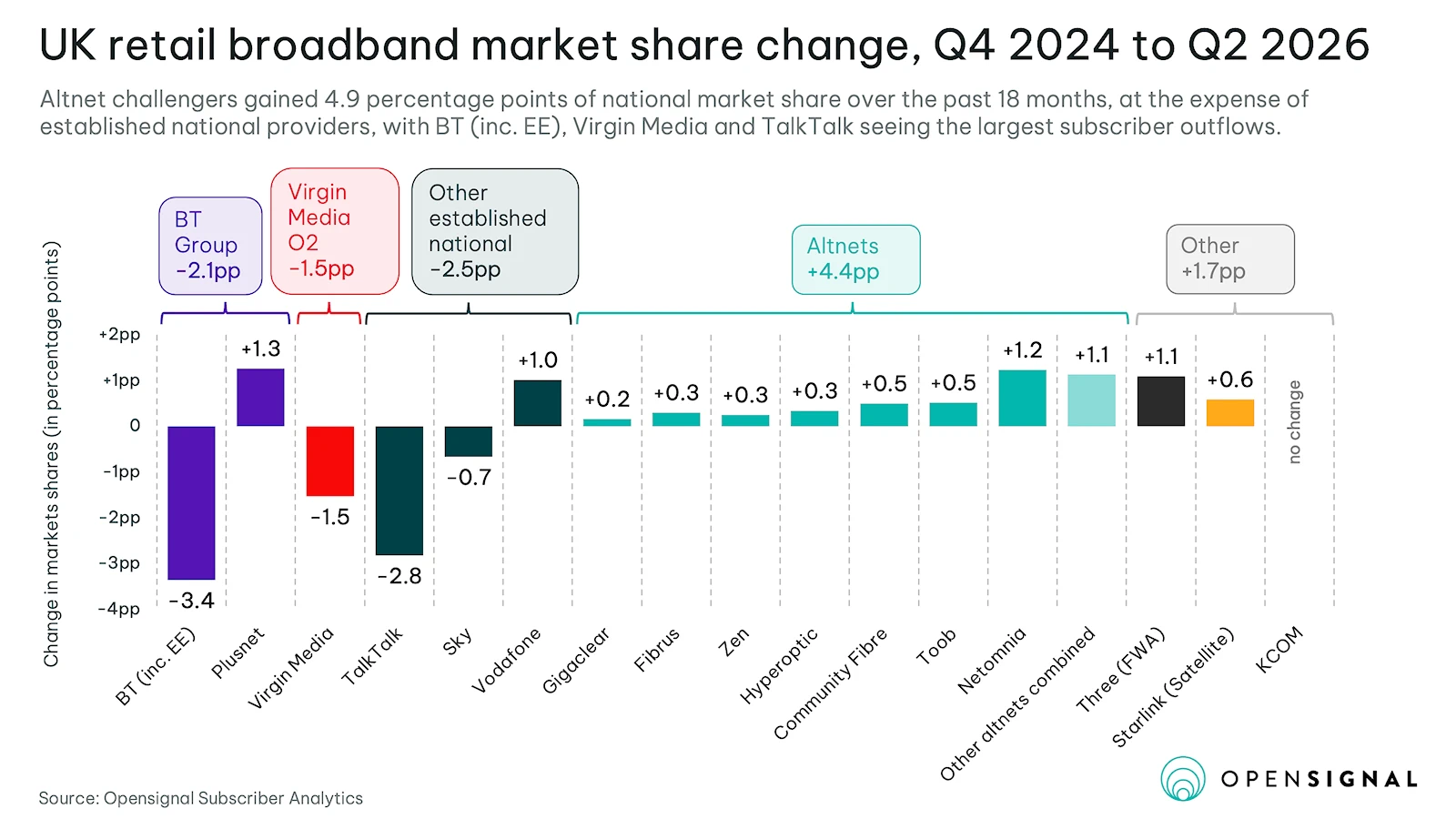

Network benchmarking firm Opensignal has today published a new report, which used device-level measurement tracking of real broadband switching (changing ISP) events across the United Kingdom to find that alternative broadband networks (altnets) grew their market share by 4.4 percentage points in just the last eighteen months (holding 11.4% of UK subscriptions).

The research – ‘Q2 2026 UK Broadband Subscriber Analytics Report‘ – reported that altnets now pass an estimated 66% of UK premises with “superfast broadband coverage” (we’re unsure how they define “superfast“, but the 66% figure appears to be based on INCA’s 2026 State of Altnets report), although the new data shows that they still account for just 11.4% of national broadband subscriptions (this closely aligns to INCA’s earlier figure of 11.9%). Despite this, the additional 4.4pp added in the last 18 months shows a strong positive direction of travel.

The degree to which altnets have an impact also varies depending upon location (some areas, such as cities and towns, have a higher density of choice than others). For example, London and Northern Ireland lead on altnet share (21% and 18%), having gained about a third of that share between Q4 2024 and Q2 2026. This pattern, of altnets recording a big chunk of their wins in the past eighteen months, holds across all twelve UK regions: the switching we are reporting points to where the market reshaping is headed.

The research also found that not all of the main incumbent retail ISPs are losing market share equally. For example, the main BT brand, which exclusively uses Openreach’s national network, fell by 3.4pp over the period and TalkTalk fell by 2.8pp (the latter has had some big challenges to overcome due to financial struggles). But others, such as Vodafone, grew their position by 1pp, partly due to their altnet partnerships with CityFibre and CommunityFibre that help to complement their Openreach base.

One other interesting observation is that Three’s 4G / 5G based Home Broadband product, which could be considered a sort of Fixed Wireless Access (FWA) package, has managed to attract a 2.9% national share – making it bigger than any individual fixed line altnet. The charts below give a good visual summary of all this.

We should point out that some of the providers in the tables above act as both retail and wholesale providers – vertically integrated (e.g. CommunityFibre both builds their own network and acts as a retail ISP, while also offering some degree of wholesale access). Similarly, others, like Zen Internet, are primarily retail ISPs that also help aggregate other altnets via wholesale for different partners / ISPs to harness. Suffice to say, it’s a complex market.

Generally, Netomnia leads the main pack of altnets with a 2.0% share (mostly via their retail ISP YouFibre and a smattering of smaller wholesale players), just ahead of CommunityFibre and Hyperoptic (both 1.7%). Netomnia is still trading independently while its acquisition by nexfibre awaits clearance by the competition regulator (CMA).

Breaking news.. more to follow..